Ohm Analytics reports an uptick in third-party ownership in several states and believes NEM 2.0 projects will support California installers for many months, while other regional market outlooks vary by energy costs and local incentives.

Multiple parties have suggested that the residential solar market would slow down in 2023 after having a very strong 2022. One quarter into 2023, the slowdown is evident, but it is showing in a more complex manner than most projected, with California NEM 2.0 applications beating industry expectations while many other states in the West and South are performing less well due to the effects of interest rates.

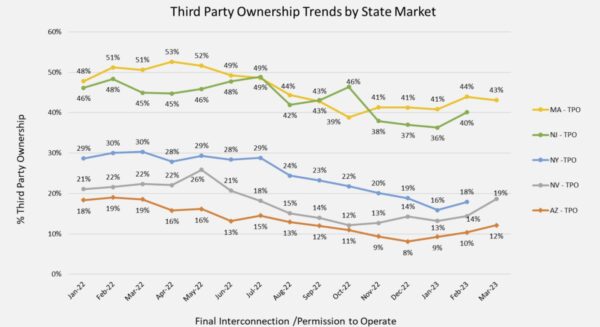

Higher rates have led to third party-financing ownership increasing in multiple state markets, according to Ohm Analytics, with Nevada and Arizona seeing increases from 8% and 12% in late 2022 to 12% and 19%, respectively, in March 2023. Sunrun also noted the strong performance of its subscription-based Shift product in the California post-NEM 2.0 landscape in its recent earnings call, suggesting that California could see a bigger rise in third-party ownership.

Several months ago, Ohm Analytics told pv magazine USA that they believed 2023 would experience slower growth. Ohm based this prediction on increasing interest rates, as well as a possible lull in California after NEM 3.0 rolled out in mid-April. However, Ohm also believed there would be regional differences due to variations in electricity pricing, incentives and installation costs, all of which influence return on investment.

During a recent conversation with pv magazine USA, reflecting back on the year so far, Ohm Analytics’ Joseph Wyer and Rohan Humphrey said that much of what’s happening in the residential solar sales market in Q1 2023 was foreshadowed in its “Q4 2022 DG Solar and Storage Market Report.”

Wyer explained,

“What we’re seeing in the data is divergent regional growth with a lot of the southern Sunbelt and Mountain States seeing slower demand on the year, initially because of the challenges around financing and interest rates, but then also some installers losing access to M1 payments. This has put financial pressures on installers, particularly in some of the southern states.”

M1 refers to the first solar project milestone payments, where traditionally a portion of the payment was paid out to the installer when the contract was signed, then another is paid after permit submission, installation, and other stages, Wyer said.

It was suggested that larger companies were reallocating resources toward solar markets with higher electricity rates or greater incentives. Humphrey said higher interest rates could result in monthly loan payments approaching or exceeding current electricity bills.

Humphrey also noted that as with all businesses, specifically in the high capital expenditure construction industry, cashflow is important to the residential solar market. Contractors that were using loan products and getting an upfront cash injection once they signed project contracts were using cashflow to finance salaries, and general business expenses. With these advance payments slowing down, cash is tighter for installers.

Sunrun and Sunnova also gain additional financial benefits from the Inflation Reduction Act and general solar finance that regular homeowners do not. As commercial entities, these groups can gain an additional 10% tax credit if they use domestic content or install in energy communities. Moreover, they are allowed to depreciate assets associated with solar projects.

One thing that surprised many was the strength of the solar market in California leading up to the end of Net Metering 2.0 on April 14, 2023. Ohm says that the number of people that signed up for solar prior to the April date are enough to build large books of business and support solar installation teams for months.

Ohm is releasing its updated market forecast and insights to customers over the next few weeks in its “Q1 2022 DG Solar and Storage Market Report.”

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

{kind=link}